How to Find the Best Types of Annuities

Annuities in general are known as financial products that shall pay out a fixed reimbursement to individuals after a certain time. Annuities were designed by financial institutions as a mean to maintain a steady cash flow. The question is how to find the best types of Annuities.

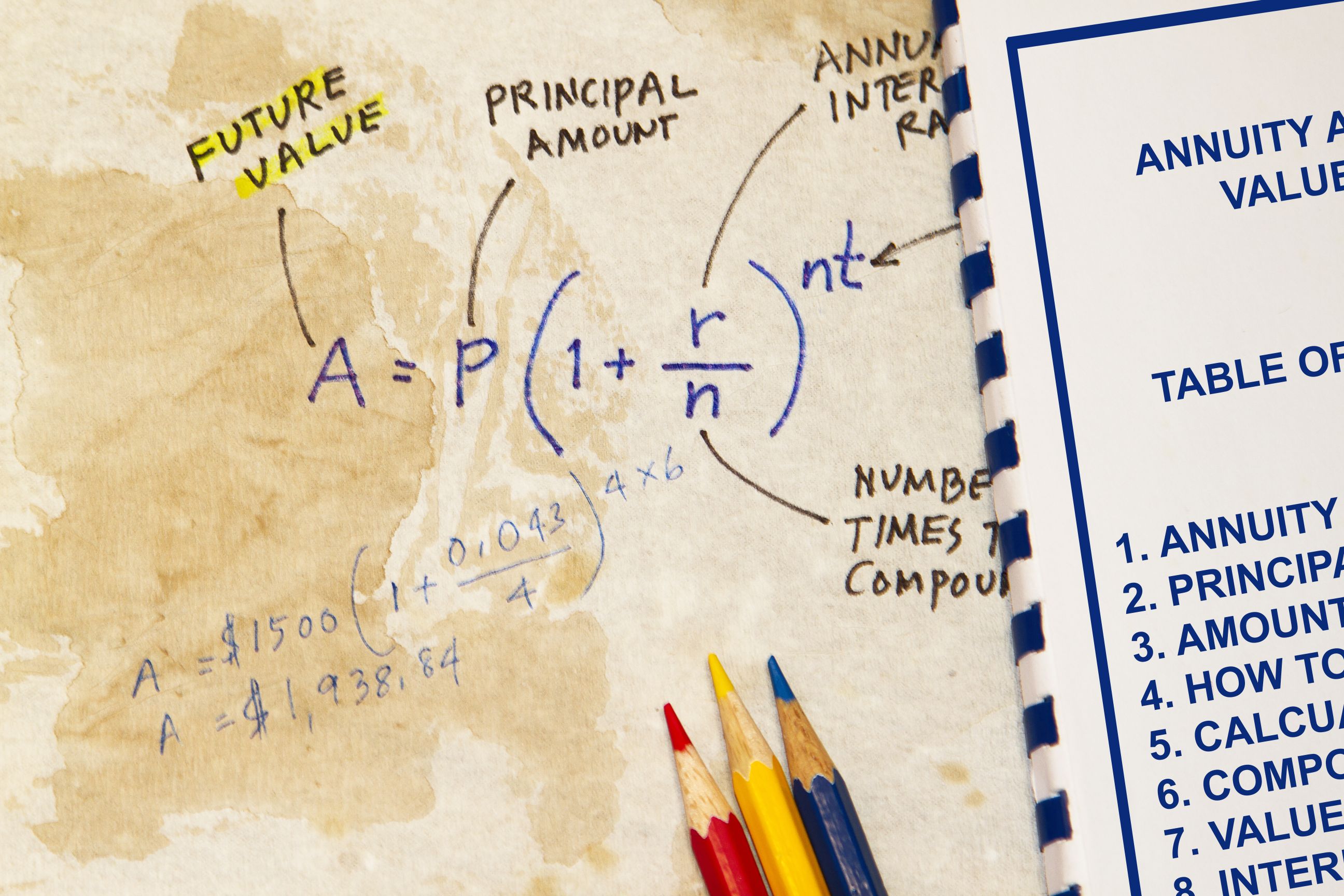

The most common form of annuity is the contract of an individual with an insurance company where they pay a certain amount in lump sum or in installments and then are disbursed after a certain time in the future.

Let us check a few type of annuities:

- Life annuity: This is an insurance product that has periodic payout till the person who bequeathed the annuity dies. They serve as providers of guaranteed income for retired individuals to live off.

- Income annuity: This is a policy initiated for prompt payments. It starts paying by the time that the policy is initiated. The income units received can be fixed or variable – depending on the plan you sign up for.

- Wraparound annuity: This is a tax-deferred annuity that provides the annuitant with some authority to control what the investment would consist of. In such annuities, the holder is not made liable to pay taxes on the annuities until the funds are withdrawn.

- Immediate Payment Annuity: This is a convenient form of annuity for anyone who has lump sum and can pay upfront. Also known as single-premium immediate annuity (SPIA), this annuity is purchased with a single payment and pays a fixed amount of income that is also initiated immediately.

These aren’t all, but one of the most common form of annuities. Which annuity is the best for an individual depends on various factors, which include:

Age of the annuity holder: The age of the buyer shall determine which annuity is most suited for them. If the potential annuitant is not healthy or is expected to live below the average life expectancy, then an immediate payment annuity will be handy for them.

The annual income: This shall mean that the annual income of the annuity holder should feasibly support the payments and installments of the annuity. Depending on the income, the individual may decide if they want fixed or variable annuity.

The financial objectives: based on the aim and objective of the potential annuitant, any annuity can become suited or unfulfilling. The applicant, the advisor and the financial institution should thoroughly workout the reason of buying an annuity and then select likewise.

Tax status of the annuitant: The tax status is of major importance as most annuities carry taxes and thus can pose burden on the annuity holder. This should be thought about and considered beforehand rather than being appalled by a sudden financial burden.

Financial experience: for anyone with relatively less experience in financial matters, annuities and their payments may become hard to understand. In such cases, one shouldn’t go with annuities that have complex payment plans – it would only torture you!

Their existing financial holdings: Any agent who recommends you to put your money in to annuities should know and be told about the fact that where your other money is invested or lies, and the form. As a whole, they shouldn’t conflict with the aim of one another.

In the entirety, there can be no one type of annuity that would be suitable or the best for all. What makes an annuity the best is its standing on the above mentioned criterion, thus it varies from one individual to another.

With litigations and regulations, the procedure of buying an annuity becomes complex. The above mentioned factors aren’t all, but are among the most important ones when making decisions pertaining to the purchase of annuities.

Category: Annuities

Business News

Popular Posts

- Cultivating Resilience and Mental Toughness - Keys to Thriving Amidst Lifes Challenges

- 50 positive affirmations to be read every day

- Mind Matters- The Chiropractic Approach to Personal Growth

- Mind Balance - A Comprehensive Solution for Navigating Modern Mental Health Challenges

- Journey Within - A Jewish Path to Self-Discovery and Spiritual Growth

- The Islamic Quest - Transforming Self for a Fulfilling Life in Allahs Light

- Buddhist Reflections - Navigating the Path of Self-Awareness and Enlightenment

- Uniting in Universal Love - Embracing Commonalities Across Faiths

- The Imperative of Unity - Why SmartGuy and Coexistence is Key to Global Survival

- Overcoming Ego and Self-Centeredness - Lessons from World Religions

- Overcoming Prejudice and Intolerance - Guidance from Global Faiths

- Cultivation and Improvement of Personality Traits to Deepen Ones Relationship with God

- How Mind Balance Can Improve the Mindsets of Employees

- Understanding Buddhism - Insights into Its Teachings Meditation and Cultural Impact

- The Essence of Islam - Understanding Its Beliefs Rituals and Cultural Significance

- A Universal Prayer for Peace and Understanding Embracing Diverse Faiths

- Cultivating Key Skills to Overcome Anti-Semitism and Hate

- How Mind Balance Empowers You Against Misinformation

- Finding Strength and Safety in Scripture - 25 New Testament Passages to Combat Spiritual Attacks

- How Mind Balance Brings People Closer to God